Domain Histories: Open Source Commercialisation

The best founders are students of history

This is Domain Histories — a weekly series mapping startup domains from first principles. The best founders are students of history. Patrick Collison met Visa's founder before building Stripe. Apoorva Mehta studied Webvan's collapse before building Instacart. They used history to make specific decisions about what to build, what to avoid, and when to move. Each issue takes one domain and gives you the full map: who tried before, why they failed, where the money sits, what's shipping now, and what a founder entering today should do differently because of it. Not a market overview. Not a research report. The history that changes what you build.

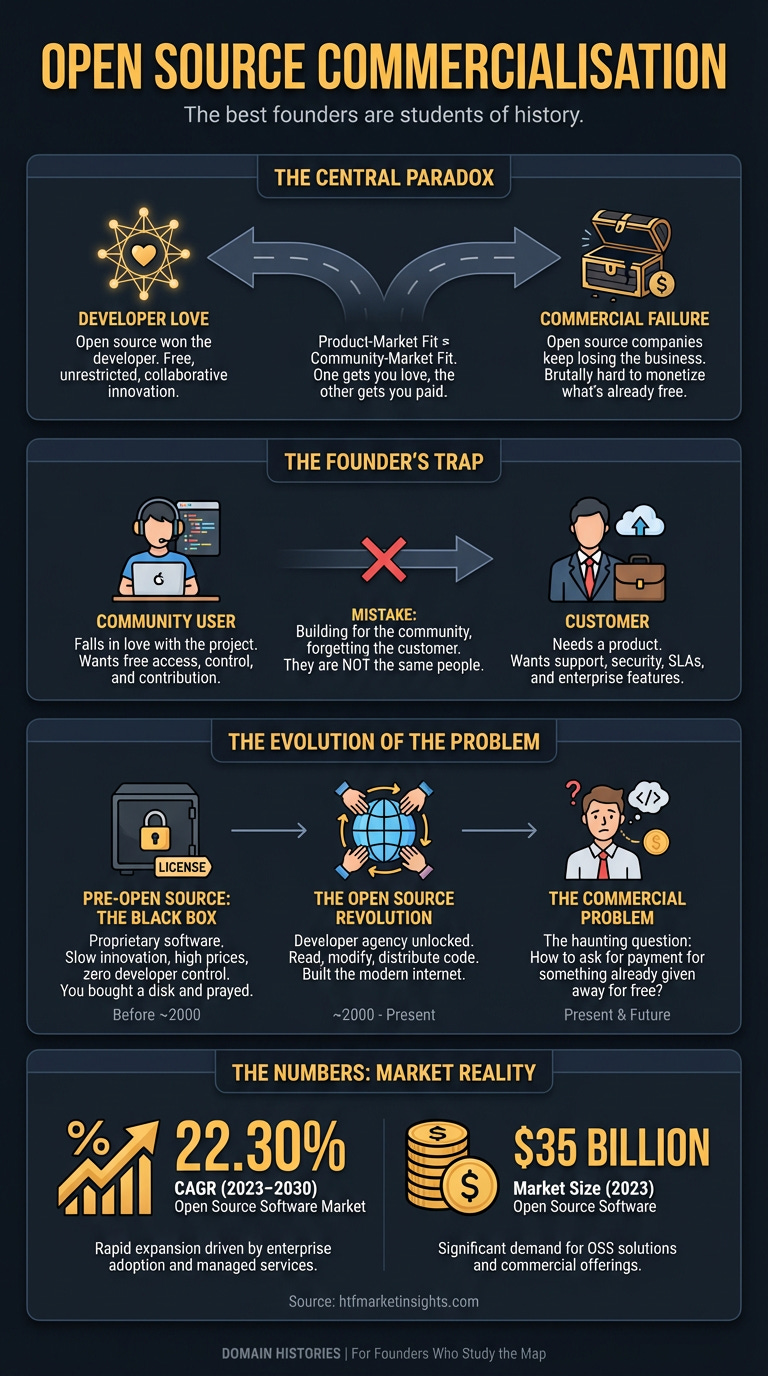

Open source won the developer. Open source companies keep losing the business.

It’s the central paradox. The very thing that makes an open-source project successful — its free and unrestricted nature — makes building a business on top of it brutally hard. I used to think a great open-source project would naturally lead to a great company. Turns out, product-market fit and community-market fit are two entirely different beasts. One gets you love, the other gets you paid.

Founders keep making the same mistake: they fall in love with their community of users, but they forget to build a product for their customers. And they are not the same people.

The Original Problem

Before open source ate the world, software was a black box. You bought a licence from a big vendor, they gave you a disk, and that was that. You couldn’t see the code, you couldn’t change it, and if you found a bug, you filed a ticket and prayed. Innovation was slow, prices were high, and developers had zero control.

Open source fixed this. It gave developers agency. The ability to read, modify, and distribute code was a revolution. It unlocked a wave of collaborative innovation that built the modern internet.

But it created a new problem. A commercial one. How do you ask people to pay for something you’ve already given them for free? That question has haunted founders in this space for two decades.

The Numbers

The Timeline

The story of open-source commercialisation isn’t really about code. It’s about the evolution of business models.

Era 1: Support & Services (The Red Hat Model) The original playbook. Give away the software (Linux), sell support contracts, consulting, and training to large enterprises that need a hand to hold. It worked. It built massive companies. But it doesn’t scale like software. Your revenue is tied directly to headcount. It’s a services business masquerading as a software business. For venture-backed startups, this model was a dead end.

Era 2: The Open Core Gambit (The Sentry Model) This became the default for a decade. You maintain a free, open-source “core” product that attracts a massive community. Then you build proprietary “enterprise” features on top — things like single sign-on, advanced security, auditing, and team management. You sell this enhanced version.

The Playbook: Build a huge funnel with the free product. Use developer relations (DevRel) to nurture the community. Convert the top 1-2% of users who work at large companies and have compliance, security, or scale problems the free version doesn’t solve.

The Poster Child: Sentry. They built an essential tool for developers (error tracking), got massive adoption, and successfully layered a commercial product on top, hitting $100M in revenue by 2024 with a lean team [GetLatka].

Why It Ends: This model creates a permanent, gut-wrenching tension. What’s free versus what’s paid? Every time you move a feature behind the paywall, you risk alienating the community that got you here. Get it wrong, and they’ll fork your project and create a rival.

Era 3: The Managed Cloud War (Now) Here’s the thing. Most companies don’t want to run software. They want to use software. The biggest headache with open source isn’t the code; it’s the operational burden of hosting, scaling, updating, and securing it.

The Playbook: The best product isn’t the open-source code; it’s a fully managed, hosted version of it that “just works”. You sell convenience and peace of mind. You are competing on operational excellence, not features.

The Great Enemy: The cloud providers. AWS, Google, and Azure are experts at this. They take popular open-source projects, wrap them in a managed service, and sell them back to the world, capturing almost all the value. This commoditisation is the single biggest threat to any open-source company today.

The New Endgame: Look at Couchbase. A veteran of the database wars, they built their own cloud offering to compete directly with the hyperscalers. Their reward? Not a soaring stock price, but a $1.5 billion take-private acquisition by a PE firm in 2025 [Matrix BCG]. This signals a market maturation. The goal isn’t just hyper-growth anymore; it’s sustainable, profitable revenue from a sticky cloud service. And private equity is noticing.

The Graveyard

Failure in open source is rarely a big explosion. It’s usually a slow fade. The project lives on, but the company built to commercialise it quietly runs out of money or gets acquired for parts.

Docker Enterprise is a prime example of an open-source commercialisation effort that struggled to find its footing. Despite immense community adoption of Docker container technology, the enterprise offering, Docker Enterprise, was acquired by Mirantis in 2019 for an undisclosed sum after raising $35M in late-stage funding.

The core Docker engine was ubiquitous, but converting that widespread use into significant paying enterprise customers for proprietary features, like advanced orchestration and security, proved challenging.

The lesson? Community love doesn’t automatically translate into enterprise revenue, especially when hyperscalers like AWS offered competing managed container services. They struggled to clearly define the value proposition of their enterprise product above the free, open-source offering, leading to an inability to monetise despite massive adoption.

Where The Money Sits

The value has moved up the stack.

It’s no longer in the code itself, which is a free commodity. It’s in the layer above: the managed hosting, the enterprise-grade security, the service-level agreements (SLAs), the 24/7 support, and the integrations.

The money sits with whoever solves the biggest operational headache for a CTO at a large company. She doesn’t care if the code is open source. She cares that it’s secure, compliant, and won’t go down at 3 a.m.

The cloud providers are the ultimate incumbents here. They are the aggregators. They take the best open-source projects and offer them as a simple, integrated service. In many ways, they are the tax collectors of the open-source economy. To win, you have to offer a managed service that is 10x better — more performant, more secure, or more feature-rich — than the generic version AWS provides through deep specialisation in areas like regulated deployments, observability, or robust upgrade and rollback guarantees.

What’s Actually Hard

The non-obvious challenge is the internal civil war.

You have two sets of users with opposing needs.

The Community: They want everything to be free, open, and unrestricted. They are your evangelists, your talent pool, and your earliest adopters. You betray them at your peril.

The Enterprise Customer: They want proprietary features, security guarantees, and someone to sue if things go wrong. They pay all the bills.

Every major decision — from pricing and packaging to your product roadmap — forces you to pick a side. This tension often manifests as dilemmas like deciding whether to paywall a feature previously available in the community edition. Companies must proactively communicate these changes, explaining the strategic necessity without alienating loyal users. Maintaining transparency about monetization decisions and actively engaging with community feedback is crucial to avoid backlash and project forks. How you manage community expectations versus customer demands, particularly around crucial features, can make or break your commercial venture.

This isn’t a technical problem. It’s a political one. Navigating it is the single hardest part of building an open-source company.

Case Study: Sentry.io

Sentry.io, an open-source error tracking and performance monitoring platform, offers a compelling playbook for commercialisation. Launched in 2010, the project gained significant developer traction by providing a critical tool freely.

Chronology and Commercial Model: Sentry initially focused on an open-source core with a hosted SaaS offering from day one. This clear split—free open-source code for self-hosting versus a managed cloud service—helped manage community expectations around monetisation. The cloud service catered to developers who prioritised convenience over running their own infrastructure.

As Sentry matured, it expanded its commercial offering with enterprise-grade features. These included advanced security, single sign-on (SSO), audit logging, and sophisticated team management tools, which are essential for larger organisations. This “Open Core” strategy meant the core functionality remained open and free, but the features critical for enterprise adoption and compliance were part of the paid SaaS subscription.

Growth and Revenue Stages: Sentry successfully scaled, reaching $100M in Annual Recurring Revenue (ARR) by 2024 [GetLatka]. This growth was driven by:

Product-Led Growth: The open-source project acted as a powerful marketing and acquisition engine, attracting developers who then brought Sentry into their organisations.

Cloud Adoption: The shift towards cloud-native architectures made Sentry’s managed service even more appealing, as companies increasingly preferred to offload operational burdens.

Enterprise Feature Development: Continuously adding features that address critical enterprise pain points — such as data retention policies, granular access controls, and integrations with enterprise tools — enabled Sentry to capture larger accounts.

Reasons for PE Involvement: While Sentry has raised $217M in venture capital [GetLatka], its scale and consistent growth (hitting $100M ARR) make it an attractive candidate for private equity. PE firms often look for stable, high-revenue SaaS businesses with strong market positions and predictable cash flows. Such investments signal a maturation; the high-growth, venture-backed phase is proven, and now the focus shifts to sustained profitability and operational efficiency through private ownership. Sentry demonstrates that a well-executed open-core, cloud-first strategy can achieve significant scale and eventual strategic exits.

Where This Goes

The next 12-24 months will see the market split into two camps.

First, you’ll have the next generation of companies following the Sentry playbook: pure SaaS, built on an open-source core, focused on product-led growth and high-margin software revenue. This is the venture-backed, high-growth path.

Second, you’ll see more established companies go down the Couchbase path. Having fought the cloud wars, they’ll seek refuge with private equity, focusing on profitability and operational efficiency over breakneck growth.

The convergence point for both is the managed cloud experience. The fight is no longer about whose code is better. It’s about who can provide the most reliable, secure, and developer-friendly hosted service. The bet is that enterprises will always pay a premium to outsource complexity and risk.

Moves Worth Stealing

The Sentry Efficiency. Sentry hit $100M ARR with a lean team, demonstrating effective product-led growth. The move? Leverage your open-source community as your primary acquisition channel and first line of support. Invest heavily in an exceptional product experience that drives organic adoption and conversion, deferring a large enterprise sales force until necessary for seven-figure deals.

The Couchbase Pivot-to-Private. Going public isn’t the only endgame. Couchbase, after years on the NASDAQ, sold to a PE firm for $1.5 billion. The move? Recognise when the public market’s demand for quarterly growth no longer aligns with your business model. A take-private deal can provide a solid return for investors and grant the operational freedom to build a sustainable, long-term business focused on profitability.

Own the Hosted Experience for Existing Projects. Don’t try to build a new open-source project from scratch. Instead, identify an existing, widely adopted open-source project with significant operational overhead for users, and build the definitive managed cloud service around it. Your differentiation comes from offering a 10x better experience in terms of reliability, performance, security, and developer tooling than either self-hosting or generic hyperscaler offerings.

The Why Now

For the first time, there are multiple proven playbooks for building and exiting an open-source company. The market is no longer just a wild frontier.

The adoption war is over. Open source won. Every company now depends on it, which means every company has the operational headaches that come with it. The demand for commercial support and managed services has never been higher. The market for commercial open-source software is forecast to reach $160 billion by 2030, growing at a CAGR of 22.30% from 2023 [htfmarketinsights.com].

The timing signal is the maturation of the exit landscape with private equity now actively investing (Couchbase, $1.5B acquisition [Matrix BCG]). You don’t need to bet on a multi-billion-dollar IPO to build a successful company. The opportunity is to find the next essential open-source project that’s a pain to run at scale and build the definitive commercial service on top of it.

If You’re Starting Monday

The Wedge: Don’t build a new open-source project. Find an existing one with a passionate community and a terrible user experience for large teams. Your product is the managed service that makes it stable, secure, and scalable. Sell peace of mind.

The Trap: Being too generous. Your free tier must be good enough to hook developers, but painful enough at scale that their boss has to pull out the company credit card. If a 100-person company can use your community edition without any issues, you don’t have a business model.

The Customer: Your user is the individual developer. Your customer is their manager, the Head of Engineering, or the CTO who is responsible for uptime, security, and compliance. Solve their problem, not the developer’s.

The First Hire: A Developer Advocate who is a respected, contributing member of the open-source community you’re building on. This cannot be a marketing person. It has to be an engineer who can write code, fix bugs, and earn the trust of other developers.

Go Deeper

The Core Tension in Open Source: On the central paradox of winning developers vs. winning business.

Sentry’s $100M ARR Playbook: The numbers behind a successful Open Core SaaS company.

Couchbase’s Take-Private Acquisition: Analysis of the shift towards private equity exits for mature OSS companies.

Open Source Software Market Forecast 2030: Market data showing the continued growth and adoption of OSS.

Mirantis Acquires Docker Enterprise: Discussion on a significant commercial open-source acquisition.

For the ❤️ of startups

Arthur is the AI native startup operating system I’m building in public — not hype, but a system that turns input into structured execution and tracks founder progress. If you want to follow or use it, it’s open for early access.

→ Access Arthur

Thank you for reading. If you liked it, share it with your friends, colleagues and everyone interested in the startup Investor ecosystem.

If you’ve got suggestions, an article, research, your tech stack, or a job listing you want featured, just let me know! I’m keen to include it in the upcoming edition.

Please let me know what you think of it, love a feedback loop 🙏🏼

🛑 Get a different job.

Subscribe and follow me on LinkedIn or Twitter to never miss an update.