⭐️ How to value your startup the way investors do

This Is How to Write Your Pitch Deck. #017a

Valuing a startup combines art, science, gut feeling and good old common sense. We understand the anxiety around setting a valuation too high, and you may fail to attract any interest, too low and subsequent rounds might see you diluted down to nothing.

We have put together help you align your needs with the reality of setting a valuation, how investors / VCs look at valuations and their drivers, and the models used to turn subjective guesswork into objective decision making.

We want to make your conversations with investors around valuations more informed and the journey far more palatable.

What’s covered:

🌟 Introduction

📜🧠 The founders truth

💰 Valuation

The maths is pretty simple

💰 So how do you work out your Valuation?

📈 The Berkus Method

📊 Scorecard Valuation

📉 Comparative Analysis

🏗️ Cost-to-Duplicate

💼 Venture Capital Method

📈💵 Discounted Cash Flow

📘 Book Value

🚦 Risk Factor Summation

🌐📊 Online valuation metrics

📝 Conclusion

🌟 Introduction

The real purpose of valuations for early stage startups is to find a split that is fair and motivational for everyone involved.

Three fundamental points need to be front of mind when valuing your startup:

What you are selling has little to no value, and your objective is to bring your vision to life. If your idea is holding on to as many shares as possible, then bootstrap.

How much money do you need to achieve your next milestone, if that means a subsequent funding round or to be able to bootstrap the business.

Will this business make investors 163x return?

📜🧠 The founders truth

If you wish to know and understand the truth behind VC and Investor motivations please read the above article to understand it is all about the money and returns.

We need to understand how to align our story, and therefore valuation, to fit their needs.

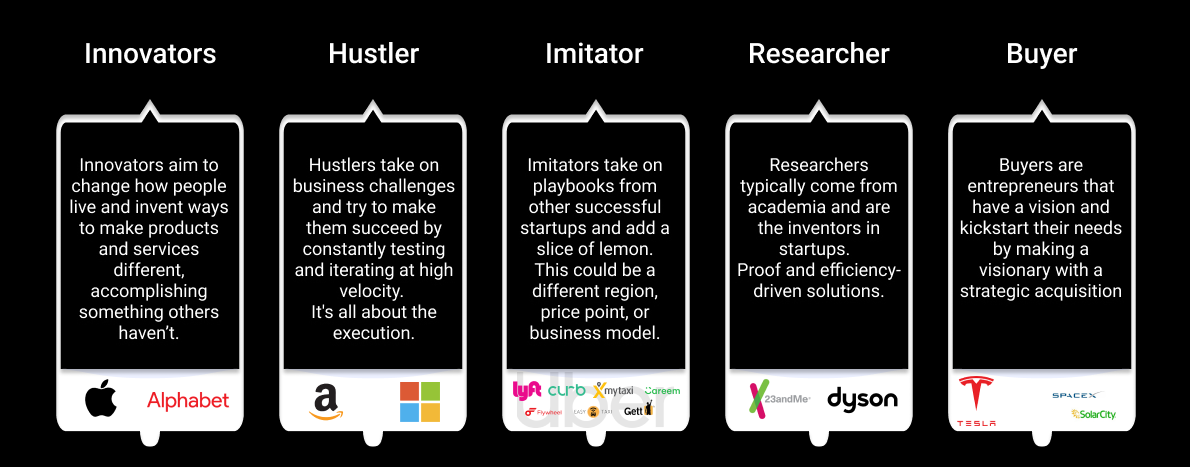

As a founder setting out to value your startup, it is handy first to identify your entrepreneur type. There are essentially five types in Tech startups, and determining which type you are will help set your goals and ask. There are no right or wrong ones, but the risks associated and pay off profile may differ between investors looking to deploy capital.

💰 Valuation

As founders we all think we have come up with the latest greatest earth shattering idea, it is very rarely the case, so getting grounded is crucial, it is also a critical part of making a realistic valuation.

So let's unpack what the fundamental objectives are for raising capital.

The capital needs to pay the bills at the Seed to Series A/B stages, as you will launch and push your product offering and customer acquisition. For this, you'll need more engineers, more marketing and sales to keep growing at the same rate; if you are exceptionally lucky, natural organic growth will kick in (this is the exception and not the rule). There will be flat spots requiring you to adjust your strategy, and as you learn more about your customer/user behaviour and fracture points, more product iterations will be required.

Many founders underestimate how difficult customer acquisition is, overestimating their internal targets. It is easy to do and all more when these KPI's are related to the growth required to attain the valuation you are trying to get.

Going into future funding rounds having overpromised and underdelivered is not somewhere you want to be.

The maths is pretty simple

A $10m valuation implies you have to reach unicorn valuation, and that the investors didn't dilute from his initial investment. Then he has achieved 100x, but that is not the case as we know that the average dilution over the early rounds is roughly 50%.

The higher the initial ask the higher the exit value needs to be, all sounds pretty obvious but is often not very well thought out.

100% of 0 will always = 0.

This is the best starting point for a founder. Selling equity in small amounts and taking in the capital that allows you to get to the next level is the best way to raise; it gives you the most flexibility and control over the direction you wish to go and increases your probability of raising future rounds. Of course using a Safe note certainly helps in averaging a higher valuation at the starting point.

One issue that always arises with founders is the fear of selling shares too cheap and being over diluted. Having the right amount of capital to allow you to hit your KPI’s will increase your valuation way more significantly than any dilution you have to take going forward. The danger with overpricing or raising too much is that if you don’t hit your targets, you’ll need to do a down round, which is always problematic.

💰 So how do you work out your Valuation?

We all have a rough idea of the market dynamics and where we sit. But investors have some capacity for their valuation because they have a mix of investments into portfolio companies.

Not all investments carry the same weight or the same conviction. To get the correct value for your company, we have put together some of the principal valuation models VC’s use when they value opportunities.

💰📊 Valuation Methods

The Berkus Method

Scorecard Valuation

Comparative Analysis

Cost-to-Duplicate

Venture Capital Method

Discounted Cash Flow

Book Value