No Distance Left to Run, Closing N2.

Why I closed it down, what I learnt and how it makes me feel.

📜 The Backstory

🗣️ What We Know Is What They Say

🔍 Understanding Market Needs

🏗️ Building and Scaling the MVP

🌐 Market Dynamics in 2021 and 2022

🎭 The Reality of Founder and Investor Expectations

📊 Evaluating Our Service

💡 Continuous Learning

💔 The Hard Truth About Matchmaking

⭐️ The Biggest Surprise

💡📚 The Main Lessons Learnt

✅ How the Choice Feels

So a couple of weeks ago I made the tough decision that it was time to close N2.

I aim to tell this story with as much intellectual honesty and emotional intelligence as possible, drawing on deep introspection and attempting to remove any personal bias.

* These are my personal experiences and may vary from yours.

* Your insights and feedback would be greatly appreciated as they help us all learn and grow.

For the ❤️ of startups.

📜 The Backstory

So here we go, N2 originally set out to be a full-service platform for private market players, covering primary and secondary market transactions. But let's kick this off from when N2 pivoted in April of 2020 to solve connecting startup founders with relevant investors.

The pivot was pretty much a necessity as we failed to raise a large enough subsequent round. I'll frame it as COVID-related because, as my favourite observation goes, the most attractive version of the truth are the lies we tell ourselves. In reality, we should have been further along in our build than we were.

There are a few reasons that I have since pinpointed, the main one being internal co-founder disputes around working methodology and objectives. It made execution incredibly difficult and in trying to keep a harmonious balance it compromised the decision-making process. We ended up building too many unnecessary features and procrastinating on the UI details, all of this added confusion made the delivery much slower, the tech team were jumping from task to task and was not able to deliver fast enough. This was exacerbated when the external pressures of COVID intensified existing differences. Unfortunately, not all team members were able to remain fully engaged during this critical period, which added to the challenges.

This sapped valuable energy and time which should have been focused on user acquisition. The pivot was a welcomed consequence which allowed us to niche down and get an MVP out to build into the bigger vision.

I doubled down on the pivot, leading the build and more importantly bringing in a new cofounder who worked with me on just onboarding users through several marketing funnels, partnerships and direct calls.

One of the critical factors in a startup team is to have shared values across all the business verticals, what execution at speed looks like, what are the attainable KPIs and timelines that can be realistically achieved but most importantly it is about being transparent and honest, where healthy discourse is welcomed and breeds a compatible working philosophy, it is a marriage after all but without the good parts.

🗣️ What We Know Is What They Say

The Pivot aimed to create a platform where startup founders could gain access and introductions to investors who could in turn receive salient deal flow based on what we know, which is what they say , not the platitudes or fluff.

One key difference is that highly regulated fund management uses precise language to describe strategies, while early-stage, loosely regulated managers often employ more forward-looking and subjective terminology.

Professional investors who manage other people's money have a thesis, a hard-coded one, it comes in the form of a legal document called a Private Placement Memorandum (PPM) or Offering Memorandum (OM), this document covers the fund’s strategy, management team, terms of the investment, potential risks, and other legal disclosures. It is the objective starting point that any founder-investor introduction should be based on.

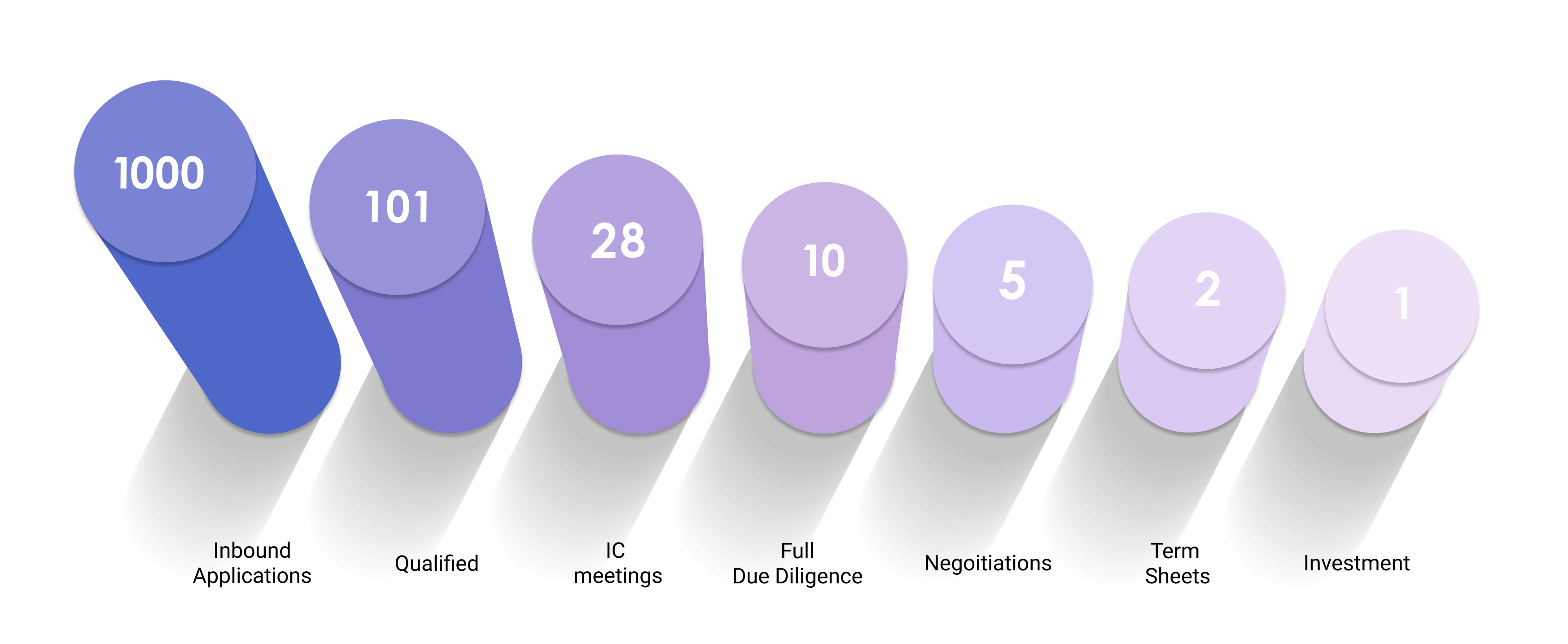

This made our job pretty clear: build an algorithm that translates what startups do to what investors do, the main qualification points being location, stage, industry, business model, domain, technology, ticket size, transformational drivers, over 500 data points in all.

Then we connected them so that every connection was based on objective relevance. The aim was to accelerate the founder's journey and reduce the investor's time qualifying their deal funnel.

The deal funnel problem was something we had spoken about with every Investor, and the issue was pretty clear, too many irrelevant and out-of-thesis opportunities, some even stated it in their email autoresponders as the reason that they may not respond to founders.

🔍 Understanding Market Needs

I felt highly motivated to address this pain point that I had lived from both sides, as an investor and startup founder, and has been a board member, advisor and raised capital for my own and many other projects, made (makes) me feel I have some very deep and unique insights into this world.

Of course, a sample set of 1 is a little delusional to base a business on, but we spoke with several 100 startups and investors to understand and validate the pain point and the easiest solution which gave us ultimate confidence we were delivering the right solution. Also, the ease in onboarding investors gave us confirmation bias, although in hindsight powered by many whimsical and false signals.

Now, being really harsh on myself after some deep introspection, I put these signals down to asking some of the wrong questions. As the famous quote attributed to Henry Ford goes, “If I had asked people what they wanted, they would have said faster horses.” I should have been building a car. 🤷🏼♂️

The lesson learnt here is in framing the questions, it is digging into the user's “why” behind the question that needs to be solved, it is in understanding the real intent of the outcomes required that drives these answers and allows us to build innovative solutions.

Unlock premium content, exclusive insights, and special offers.

🏗️ Building and Scaling the MVP

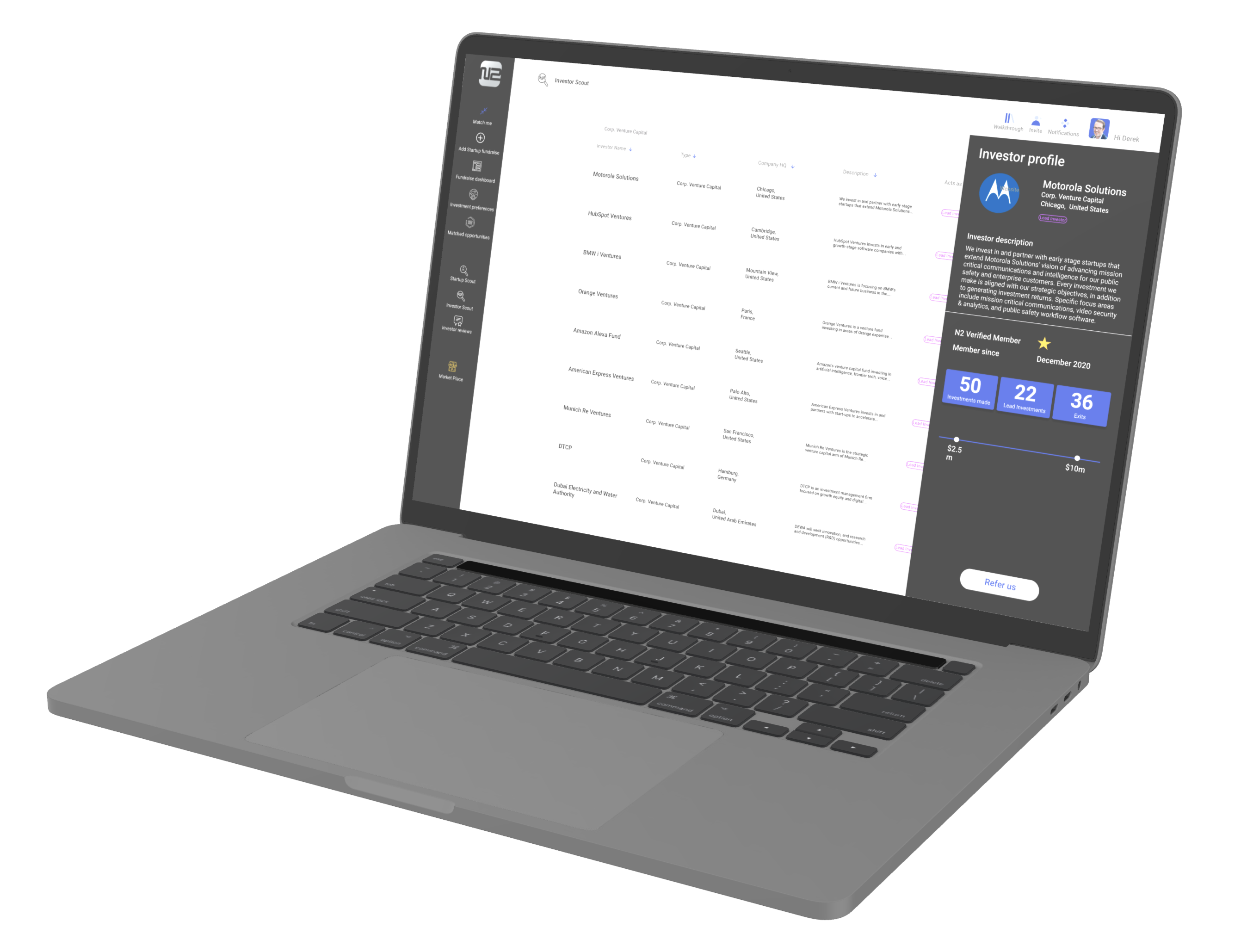

We started building a dirty MVP in the May of 2020, hacked it together using gaffer tape, and launched in August ... a week in with just 100 or so verified investors onboarded (meaning we had spoken with them and made sure they actually had cash to deploy into new opportunities) we got our first paying startup customers... traction.... a glimmer of hope?

Well, it carried on like this, by December we had over 250 investors, got some interesting onboarding stats around this (more on that below 🤪), and had generated about $20k in revenue. Startup growth was at around 6% a week with a conversion rate of 15%

Although 2020 with the onset of COVID brought a massive collapse in markets and VCs triaging their portfolios into the good, bad and ugly, we have to remember we were in a free money environment of massive stimulus packages being printed in a zero interest rate environment so however bad things were the risk appetite was monumental.

For N2 it was exciting times and positive signals, so much so that we thought we had better up the UX somewhat to something a little more professional, the previous onboarding and uploading forms of the dirty MVP looked like something I had written in Visual Basic from the '90s.

🌐 Market Dynamics in 2021 and 2022

The market in 2021 was kind of great, even with all the disruption of COVID, Spacs were being issued like there was no tomorrow, an apt expression in hindsight, money was being poured into anything deemed 'Pandemic-Proof' like remote work solutions, health tech, e-commerce, and edtech.

But as 2021 progressed, the landscape began to shift. The inflation cycle was starting to be felt and rumoured interest rate hikes were becoming an imminent reality. Supply chains were being disrupted and Investors started becoming more selective, focusing on profitability and long-term viability rather than just growth metrics or pandemic-related opportunities. The flood of stimulus money that had buoyed markets began to ebb and conversations around funding were becoming ever tougher.

2022 saw more of the same with the expected aggressive rate hikes being implemented, but other things started hitting the industry. Added to this was the start of a major conflict between Russia and Ukraine and the disruption to the banking system it brought, the venture market experienced a significant cooldown in 2022, the most relevant events were the heavy markdowns across the board after seeing previous darlings like Instacart, Klarna and Stripe doing down rounds at more than 50% discounts to their previous rounds. The collapse of the Terra (LUNA) UST stablecoin in May and the FTX exchange in December contributed to the negativity.

These events, combined with the loss of hundreds of thousands of jobs in the tech industry, continued to have a slowing effect on investment appetite and startups coming to market in general.

But on a positive note, at the end of 2022, we saw the huge launch and uptake of OpenAI’s ChatGPT but as we entered 2023 we started with the collapse of SVB and the knock-on effect was felt globally.

The biggest issue on N2 as a business was the amount of events, both positive and negative and it was mainly felt on the investor engagement side of the market. Having to manage global situations of the magnitude we saw for relatively inexperienced investors sitting in small boutiques is uber tough. The noise around AI was overwhelming and of course forced investors once again to triage their portfolios and see who was AI-ready, understanding how it would affect their portfolio companies.

🎭 The Reality of Founder and Investor Expectations

The founders takeaways:

Chasing Funding and Access

Founders' initial expectation is straightforward—they want quick and easy access to investors who are ready and willing to invest. Yet, the path is not as direct as they hope. Each step towards an investor is critical, but it’s just the beginning of the journey.

The Harsh Reality of Introductions

While our platform provided access to investors there is no magic pill to getting funding. No intermediary—no matter how efficient or connected—writes the cheques, that is always the ultimate decision of the investors. A truth that every founder must understand is it is on them 100% to sell and close.

Empowering Through Understanding

I often considered going down the education route, thinking that building a successful marketplace for startups isn't just about making introductions. It's about empowering founders with a deeper understanding of the fundraising process. It's about preparing them to understand that investors are default 'No'. But I do not believe this to be the case or utility of a platform, any platform where humans are overly involved in the process is by default not scalable. We aimed to streamline this reality, build trust and credibility not by sugarcoating it, but by accelerating the journey to a clear answer.

Therein laid a critical insight, the naivety, ego or overconfidence of founders getting 'No's was not a function of their business but a function of investors and by association our platform.

The Investors takeaways:

For investors, using our platform marked a shift from a quantity-driven approach to one emphasizing quality and precision. Many investors traditionally operate with a broad, somewhat haphazard funnel, often relying more on serendipity than strategy. This 'catch-all' method can sometimes serve to enhance an investor's social visibility or even act as a vanity metric, signalling their status as a go-to VC in the ecosystem. This rhetoric of ‘we see 1000 deals a day so we have access to the best’ is just an attempt to raise their social capital, a tool then used when doing LP beauty parades, but it is just a mind-numbing manual curation task when there are way more important tasks at hand.

Dynamic Engagement and Real Outcomes

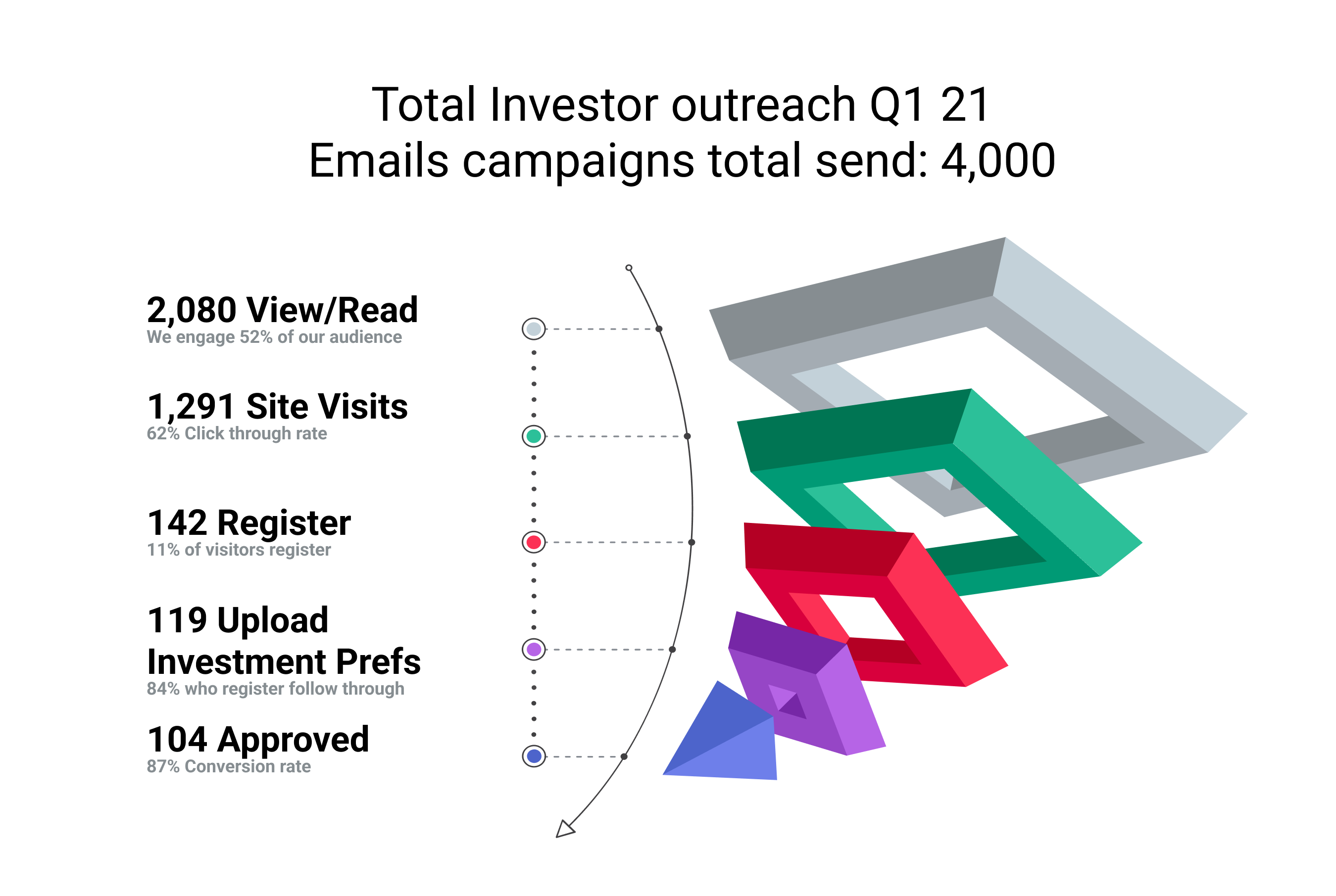

Our platform's ability to provide targeted connections led to astronomical engagement rates, with some periods seeing investor interaction as high as 85% on shared opportunities. This high level of engagement was not just a statistic but translated into real success stories: from a Series A startup securing a call with a corporate VC within an hour to another receiving a term sheet just a week after introduction. These successes set high expectations, both internally and externally, reinforcing our platform's effectiveness.

But building a successful marketplace for investors that keeps them engaged, using and championing the platform consistently is difficult. Raising access works both ways, making it easier for founders makes it less exclusive for investors, and dilutes one of their proclaimed edges over competition, their network and access to deals.

Therein laid a critical insight, how do you level the playing and change the game without playing by the obvious rules of the game?

📊 Evaluating Our Service

For N2, despite the strong start with great initial traction, we exposed some critical challenges. Our growth rate, although steady, wasn't accelerating at the necessary pace needed to generate enough free cash flow to lower the burn rate or to secure further funding rounds in a way that I would feel comfortable doing.

By the end of 2022 we had onboarded over 3000 startups and close to 800 investors (4200 and 850 end of 2023) had been verified to receive deal flow from us. But, a big but, our burn was too high to maintain operations and I cut the tech team back to the bones and carried on to figure out other marketing and sales channels.

We pushed out newsletters and online marketing campaigns, made partnerships with associations, incubators, and accelerators and managed to get some consistency, but looking back we were limited in time to have any efficiency. Even with plans and processes in place, scaling was painful and the more we scaled the harder it got.

Conversions, (startups paying) although around 12% to 15% for such a service that makes connectivity to relevant investors immeasurably faster might seem good. I believed it was mediocre at best and solving for this before loading up more numbers was front and centre.

Investor interactions were also not high enough, although we knew that the pipeline we created for them was substantially cleaner the reliance on them updating their preferences to maintain relevance became a manual time-consuming task of chasing them and to keep them engaged and simply give startups feedback with a single click (although they did have to log in to see the opportunity to engage) was something we struggled to solve and a major challenge.

The consideration to transition to a SaaS model loomed large. Should we have started charging a modest monthly fee? My deliberation hinged on whether we first needed to bolster user engagement. However, I haven't settled on a definitive answer. Part of me still believes that introducing a fee might have stimulated greater commitment and consequently, higher engagement. Yet, the challenge with an MVP is its inherent feature limitations, making it difficult to develop a SaaS product that effectively engages and retains users.

💡 Continuous Learning

To deeply understand some of our challenges at N2, I continually immersed myself in the ecosystem.

Mentoring at Universities, Incubators and Accelerators to see, hear and learn the challenges being faced and the solutions being offered.

I quickly concluded that to wear a mentoring badge you didn’t have to qualify or have any experience as a Founder or Investor. To fulfil the desired needs of attraction through big numbers and shiny objects all that is required is the ability to regurgitate quotes from Zero to One, The Hard Thing About Hard Things and become a specialist on what Y-combinator says.

Consensus head-nodding rules and the HOW to get shit done is literally never spoken about.

We also started a new initiative Fundraise as a Service (FAAS) to achieve a several things.

Earning money to pay the bills is always a good idea.

Educate founders on the requirements needed to fundraise and deliver solutions.

Split the startup journey into key area, learn from the experience to build digital products.

Investor leanings

On the investor side after 1000s of calls, I started to mentally categorise and then fully document them, they fall into these main categories.

You have the real adventure capitalists, they have such a strong view of the future and understand what is required to join the dots to get there. They might be wrong, they might be right in the long term, but they have 100% commitment to their view.

You have the specialists, they know their stuff deeply and have an incredibly strong thesis. They understand business, they understand how to make shit happen and what value they bring to the table.

Then come the generalists, the majority and the biggest grey area, they want to be specialists so proclaim to have a strong thesis which will be one industry, domain, model, or tech vertical that you can squeeze anything into if you squint, and it changes when the wind blows as they learn. Some, the majority, are intellectually honest and understand where they are at, some think that being committed to the art of the “world's biggest a-hole” is the winning formula. These generalists are the most relatable as they act and appear like Startup founders because they are.

Then come the FOMO sheep, you can see them a mile off, and they can name every new startup in the hottest sector of the moment. Good and bad actors here. The good are just trying to make their way, learn on the fly and are pretty open about their limitations. The bad, well they are like pump-and-dump bandits, straight out of the Wolf of Wall Street.

The sheer volume of experiments we have run over the period has led to some incredibly powerful data-driven insights, from testing the data of all the main investor detail providers to investor outreach programs at scale to measure email engagement, response times, and answers.

We even ran an analysis to understand if what investors say versus their portfolio companies is aligned, you would be very surprised at the range of correlation.

Some of the more psychological findings is how much groupthink exists around totally subjective issues to pure repetition of tasks hoping for different outcomes, is that not the definition of insanity?

💔 The Hard Truth About Matchmaking

Investor onboarding and keeping their preferences up to date was perhaps the biggest challenge, a manual process in pursuit of quality over quantity. Those social media posts with here is a list of 50000 investors drive me nuts, out of date second-hand stale data clickbait.

Every new investor onboarded was a manual telephone call to introduce the value proposition and ask the hard questions founders rarely do. The most interesting statistic from the “Do you have moola in the cooler for new investments” was a staggering 35% were either raising a new fund or only had follow-on cash. Yet, as this is not public information they still take calls with founders to be in the market and gather intelligence, no shame in wasting founders' time, just spin it as good experience and put me on your mailing list.

This I get fully, gathering intelligence is a key part of an investor's job, they need to understand where the market is, what is changing, what is coming, and how other investors are viewing the market.

The issues around how it is gathered are the premise for founders to give their time and information is based on investment. Secondly, it is used to play a knowledge arbitrage game, sometimes just to inflate social capital but more surreptitiously to give their portfolio companies an advantage.

Another problem lay in getting investors to look at the deal flow they were receiving, typically the pattern was always the same, active for the first 10 to 15 deals and then a gradual decline to just looking but not bothering to respond to founders, to then just not bothering. What can we put this down to?

The deals are in their thesis but not ticking some of the subjective in-house boxes required.

This was super relevant and part of the roadmap to build out more.

Too busy, too much other deal flow to bother looking at ones that fit.

Quantity over quality.

Wanted the deals in their systems and not log into another platform.

Have in-house systems for processing deal flow.

Fit the thesis but the quality of the previous deal was not high enough.

Bit of a head-scratcher, but expectations are super high and want someone else to do the diligence.

Another clearly identifiable problem was our communication flywheel. Remaining front and centre when delivering curated deal flow means less opportunity to be front of mind. Although we had different parts working it was not personalized or localised enough to garner the interest required. Also giving tools that rely on users being the fuel of the flywheel is a wish and prayer. Nurturing each step is key for engagement as I now believe being omni channel is.

😀 Some of the things we had to deal with

Trying to identify the problem with founders converting was a priceless learning experience., In some cases, it was price-related, in a lot of cases it was a lack of understanding due to the amount of people offering zero-cost services and just spraying and praying for a success fee. Because of these bad actors a culture of questions such as “What are my chances of raising ?”, “is it guaranteed”, and “Can I pay you once we have successfully raised?” has been instilled in founders.

Let's break Price related issues down a little more:

➡️ To add a little context we only dealt with Seed to Series B raises, so here is my take on a founder saying $799 for pay-to-play introductions to relevant investors is too expensive.

Here are the minority reports:

Too expensive.

The founder is undervaluing their time as the manual process of doing this is many hours over many weeks, on an hourly rate the $799 we charged is so ridiculously cheap.

I understand for many it is a large slug of money, but frankly if at the seed stage, this makes such a massive dent in your balance sheet then the chances of raising are incredibly limited.

Founders have a huge confirmation bias that leads them down a road of thinking that just getting in front of an investor they will raise.

What are my chances of raising?

There are a few answers to this;

Higher than people not reaching out to relevant investors.

I have no idea because for 800 bucks I am not going to study your startup to come up with a finger-in-the-air number.

0.5% like everyone else's because there is a finite amount of money allocated to be invested into Startups and platforms can raise the probability of having access to try and raise but not the overall amount allocated.

Is it guaranteed?

“Yes, 100% that you will be introduced to investors cause that is what we do.

“No, is it guaranteed I raise?”

Whoever said a job can’t be fun and make you belly laugh needs to get on some of these calls, they make Ricky Gervais seem like Pope Francis. (not sure I am allowed to say that, but I have)

Pay on successful outcome

“Can I pay you once we have successfully raised?”

“What does your startup do?”

“We are a 1 minute food delivery platform.”

“Great, can I order and pay you once I have successfully enjoyed eating what I ordered?”

“No you have to pay when it is delivered, it's a delivery service?”

“Ahhh ok thank you, what was your question again?”

Or this one, I only got matched with two investors, I am not paying $800 for that?

Good, because the price is now $5000 per intro. Finding those two relevant investors is going to be tough.

These are the minority reports of course, but some of the frustrations that we, and every founder has to go through when doing something different from the status quo.

What is the root cause of the issue? The inherent belief that it should be a free service? Afterall it does answer some pretty serious pain points for founders, it is 10x faster, 10x cheaper (calculated versus a founders time) and 10x more efficient, you get answers so much faster.

The startup world has been so Googlised and Techcrunched to the point where our common sense doesn’t work.

Since when is searching for something and being told that you have 8,465,832 results in .004 of a nano second a good thing?

Since when is Bob and Sally raising $10,000,000 on an idea written on the back of a napkin a reality for all?

A world of bright lights and shiny objects with immediate dopamine hits is what we face(d). We got our fair share, 80% of Series A founders got it, they were more along the lines of, what seriously, $800 …. Done.

⭐️ The Biggest Surprise

The biggest surprise for not converting what I deem as serious founders and not wannaprenuers was this, at the end of the user journey before payment, users would land on a page that would display 3 of their matches;

a large household name like A16z or Sequoia,

the next is a local VC

a more off-the-wall investor, maybe a family office or specialized CVC, a name most founders would not have come across.

But this was by default the biggest issue, this gave founders some anxiety, normally along the lines of we are not ready, we are gonna blow our chances with Sequoia.

Now this can be looked at in a couple of ways.

I get it, but are we ever ready? What you send today is not a door number and tomorrow will have evolved anyway.

It is safer for one's ego to do it from our own email account, that way nobody ever has to know if we fail. (if we actually ever do press send)

💡📚 The Main Lessons Learnt

I am saying these in a very binary way but only to get my point across, of course, I understand there are caveats to all of these.

Never go 50 50 with a cofounder.

There has to be a leader to make the hard calls when they are needed. It is not a little consensus voting system based on minority rule that is needed at the startup stage. It is a team attitude where one person takes the best ideas, takes responsibility when they go wrong, and hands out gratitude and celebration to the right team or person when they go right.

Never give for free.

If you value what you are delivering and believe in the value-added, never give it for free. It makes users lazy and disrespectful. Users stop using something that has no $ value assigned to it if it doesn’t have immediate results. (sales cycle)

Communication and flywheels.

I can’t emphasize how hard it is to build consistency, see all the right triggers, add value and deliver. It is perhaps the most important tool to remain front and centre.

Do not rely on 1st party data go way more data-driven.

User form filling goes out of date very fast and updating it cannot be relied upon. Zero-party data holds more insights than you can imagine if understood and used correctly.

Resilience rules.

It is incredible what we can achieve

Build with easy access to your data.

Data-driven insights are the power to decision-making at speed and scale. We spend so much time thinking about the user experience and not enough about internal process times.

✅ How the Choice Feels

So there we have it, the lived experience of trying to make the startup ecosystem less opaque. The hard thing about building a marketplace is they are F******* hard.

❓ Is it failure? well certainly from the investors’ standpoint who put money in and came away with nothing, me being one of them, of course on that metric it is a total failure. With that comes gratitude to those who believed and backed it and disappointment for not having overcome the challenges.

But failure, no, because closing it is a choice based on logic and not despair. I have gained so much value from this journey and learnt so much, met so many outstanding people that in large I am just grateful.

Here are the logical points that drove the final decision.

Our MVP Tech stack has reached its limitations and the tech debt is too high.

What is needed from a tech POV considering access to AI models, we would need full reengineering.

The cost of maintaining versus time and resources to give a fair and proper service means the squeeze is not worth the juice.

Times have changed too much and my overall view of platform solutions has changed dramatically.

A lot more on that to come.

One question I often ask myself

do I still think the truth I believed in is still the truth?

And that is a 100% yes, there is a huge problem to solve

For the ❤️ of startups

✌🏼 & 💙

Derek

Thank you for reading. If you liked it, share it with your friends, colleagues and everyone interested in the startup Investor ecosystem.

If you've got suggestions, an article, research, your tech stack, or a job listing you want featured, just let me know! I'm keen to include it in the upcoming edition.

Please let me know what you think of it, love a feedback loop 🙏🏼

🛑 Get a different job.

Follow me on LinkedIn or Twitter to never miss an update.

The most interesting statistic from the “Do you have moola in the cooler for new investments” was a staggering 35% were either raising a new fund or only had follow-on cash. Yet, as this is not public information they still take calls with founders to be in the market and gather intelligence, no shame in wasting founders' time, just spin it as good experience and put me on your mailing list.

I feel silly asking this (as though I need permission to ask a question) but I'm curious if that's something a founder can/should ask up front? Or just take the call and charge it to the game in a matter of speaking.

"You have the real adventure capitalists, they have such a strong view of the future and understand what is required to join the dots to get there. They might be wrong, they might be right in the long term, but they have 100% commitment to their view."

In your experience, do they self-identify as such? Or do I need to become a canyoneer to make their acquaintance? #canyonsarethenewgolfcourse