The Trillion-Dollar Loop: How Circular Capital is Building AI's Future

Part 1 of 5: The Great AI Infrastructure Build-Out of 2025

There’s a peculiar transaction at the heart of the AI boom that should make you pause.

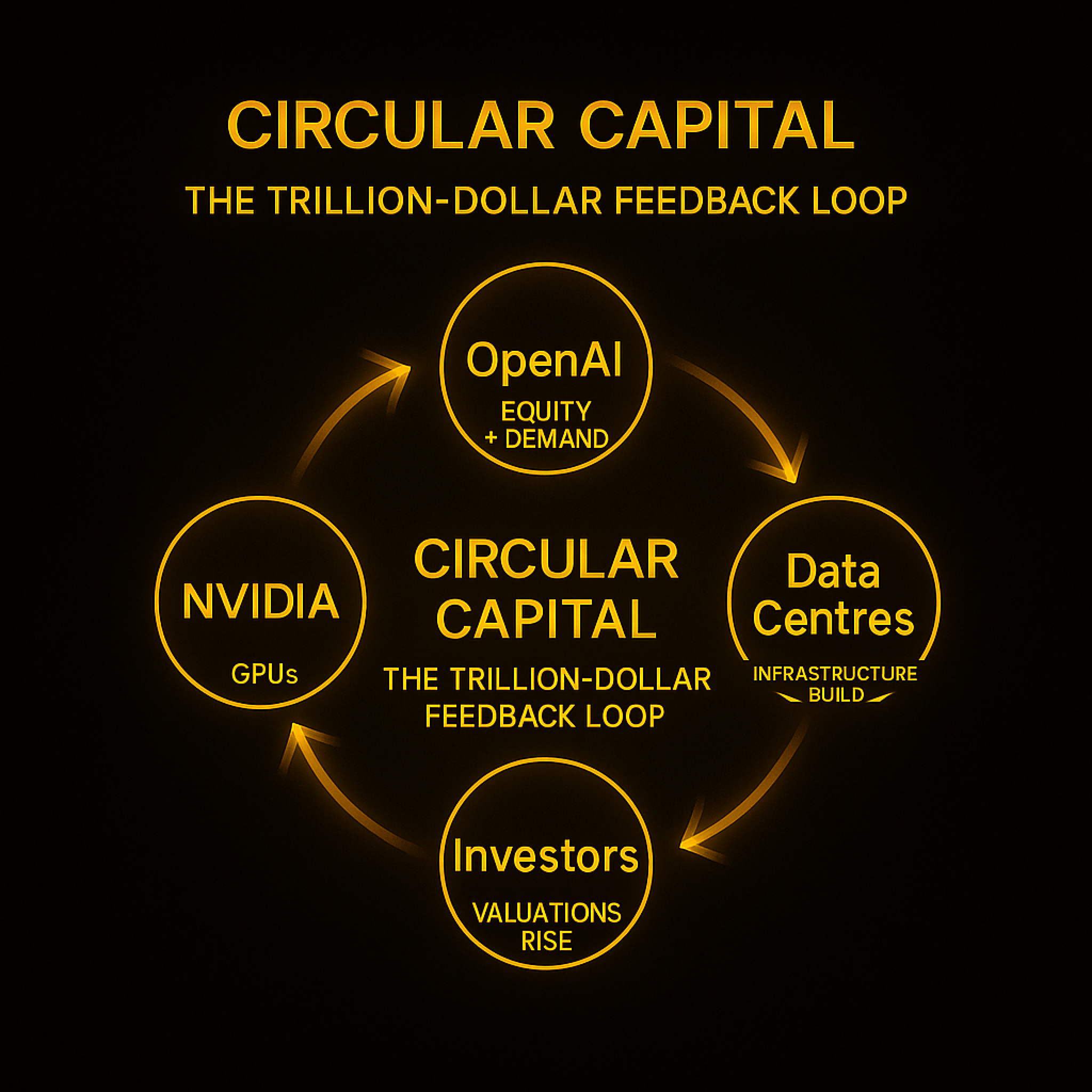

NVIDIA agrees to invest $100 billion in OpenAI. But it’s not writing a cheque. Instead, it’s supplying GPUs—the very chips OpenAI needs—in exchange for equity. OpenAI uses those GPUs to build data centres. Those data centres need more GPUs. NVIDIA supplies them. The valuation of both companies rises. More investment flows in. The loop accelerates.

If that seems circular, it should. But is it dangerous—or exactly what an early infrastructure build-out requires?

In 2025, a trillion-dollar investment frenzy has swept AI, bankrolling everything from cutting-edge chips to massive data centres. Private investment in AI by U.S. firms alone reached $109 billion—about 81% of the global total. NVIDIA briefly joined the trillion-dollar club as GPU demand surged. Foundation-model startups saw valuations leap into the tens and even hundreds of billions, virtually overnight.

Unlike software booms, the 2025 rush is an infrastructure build-out—expensive, large-scale, and entangled with geopolitics.

This is how circular capital is constructing the substrate of the Intelligence Economy. To judge innovation vs instability, distinguish three often-conflated mechanisms: strategic ecosystem building, vendor financing, and asset-backed lending—each with different risk profiles and economics.

🧲 The Tension We’ll Resolve: Why Build Infrastructure That Rusts?

Before the mechanisms, the elephant in the room: GPUs are obsolete in ~3 years, not 50 like railways.

A railway laid in 1850 was still running in 1950. Fibre laid in 2000 still carries traffic today. But an H100 cluster from 2023 is already being replaced by Blackwell in 2025.

So why is rational capital funding infrastructure that won’t last?

Three possibilities:

Solving coordination problems (rational short-term strategy)

Betting AGI arrives before depreciation matters (15% probability)

Collective delusion (most likely)

For now: fast depreciation is the variable that makes everything else either genius or insanity.

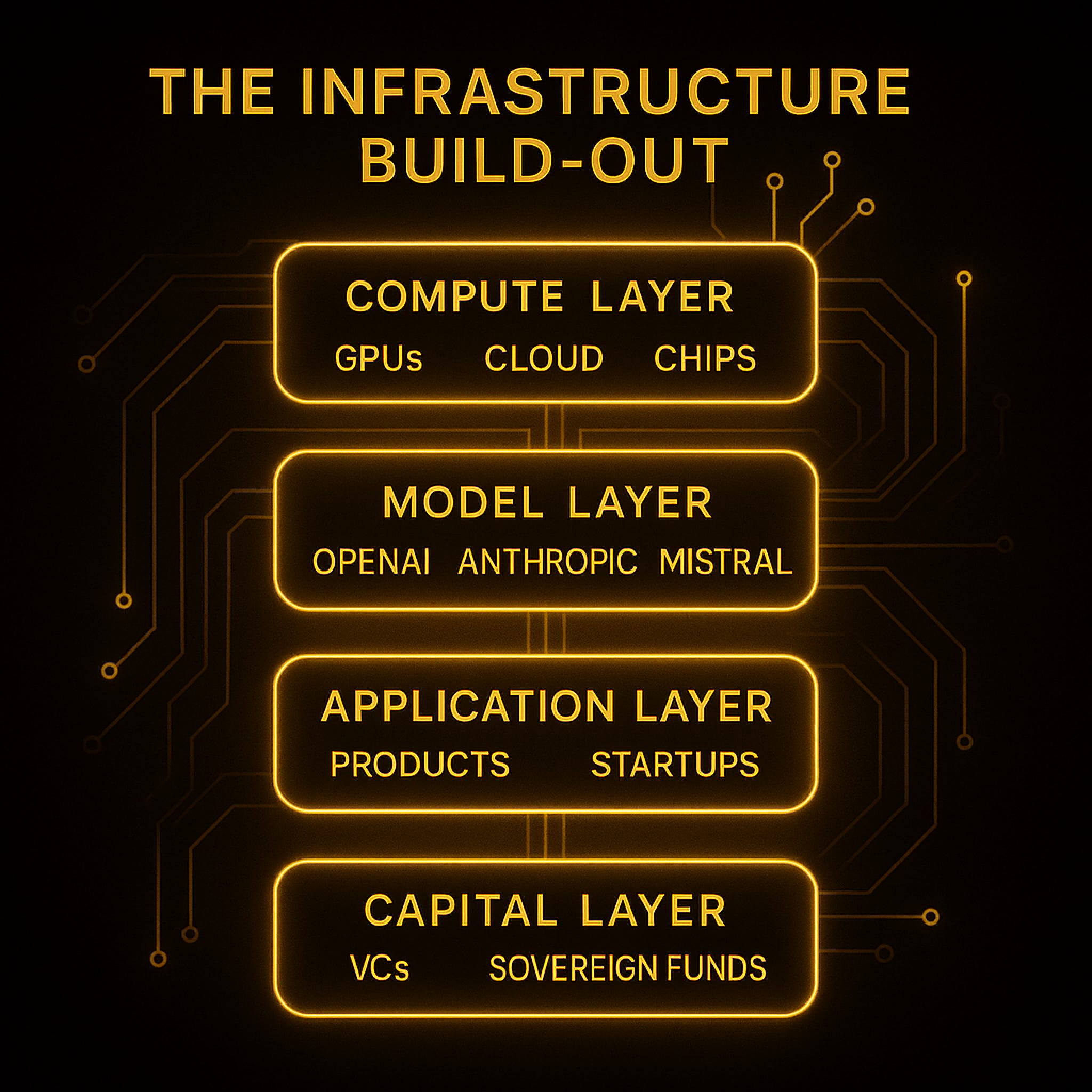

💱 Compute as Currency: The New Rules of AI Finance

In 2025, compute isn’t just a resource—it’s a currency. Startups raise in-kind capital via GPUs and cloud credits, blurring vendor and investor.

Consider Inflection AI’s $1.3B (mid-2023): a mix of cash and cloud credit, valuing it at $4B. Credits on Azure enabled a planned 22k-H100 supercomputer—~3× GPT-4’s training compute.

This is now the standard playbook.

Clouds seed startups with compute: e.g. Google Cloud offered YC startups priority Nvidia access plus $350k credits—fuel for development in exchange for platform lock-in.

Message: to build in AI you don’t just need money—you need GPUs. Those who control GPUs control access to the future.

Is that circular—or simply smart allocation under extreme coordination constraints?

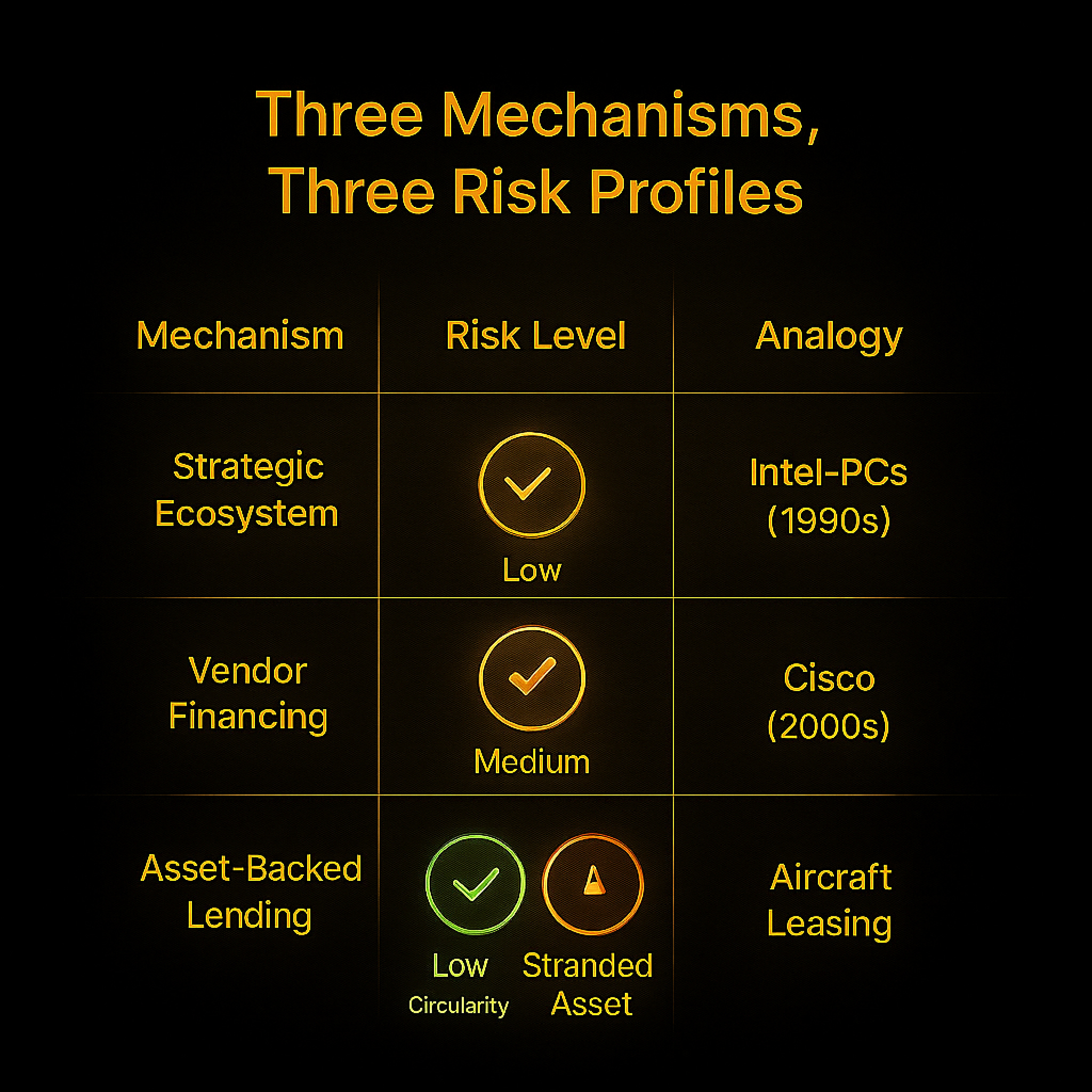

🧰 Three Mechanisms, Three Risk Profiles

1) Strategic Ecosystem Investment (Rational, Low Circularity)

A platform invests in firms that drive demand for its platform; capital is external; the thesis stands alone.

Example: Microsoft’s $10B in OpenAI (2023) via Azure credits + equity.

Risk: Low circularity (strategic, not structural).

Parallel: Intel → PC makers (1990s).

2) Vendor Financing (Questionable, Medium Circularity)

Supplier extends credit/takes equity so customers can buy its product; revenue depends on its own financing.

Example: NVIDIA’s ~$1B across ~50 AI startups (2024); $160M lifeline for Applied Digital.

Risk: Medium circularity—loss of equity and revenue pipeline if customers fail.

Parallel: Cisco in the dot-com era.

3) Asset-Backed Lending (Rational, Low Circularity — High Stranded-Asset Risk)

Debt collateralised by GPUs; lenders bet on cashflow + resale value.

Example: CoreWeave $2.3B GPU-secured facility; >$11B AI hardware ABS by 2024.

Risk: Low circularity, but high stranded-asset risk if oversupply, obsolescence, or 10× efficiency gains hit.

Parallel: Aircraft leasing—robust until shocks; GPUs depreciate far faster.

🛡️ The Steelman: Why This Might Be Optimal

Coordination: Platforms (MSFT/GOOGL/NVDA) have the best demand signal and can coordinate the build-out via in-kind capital.

Information Advantage: Clouds/chipmakers see usage and traction in real time—better signal than most VCs.

Vertical Integration: Chips + infra + models + apps need ecosystem capital and distribution, not just cash.

Bottom line: If AI infra is transformative, demand materialises in 3–5 years, platforms have superior information, and coordination is required—then circular capital is a feature, not a bug. The real question is whether those assumptions hold.

⚠️ Where the Real Risks Lie: Three Failure Modes

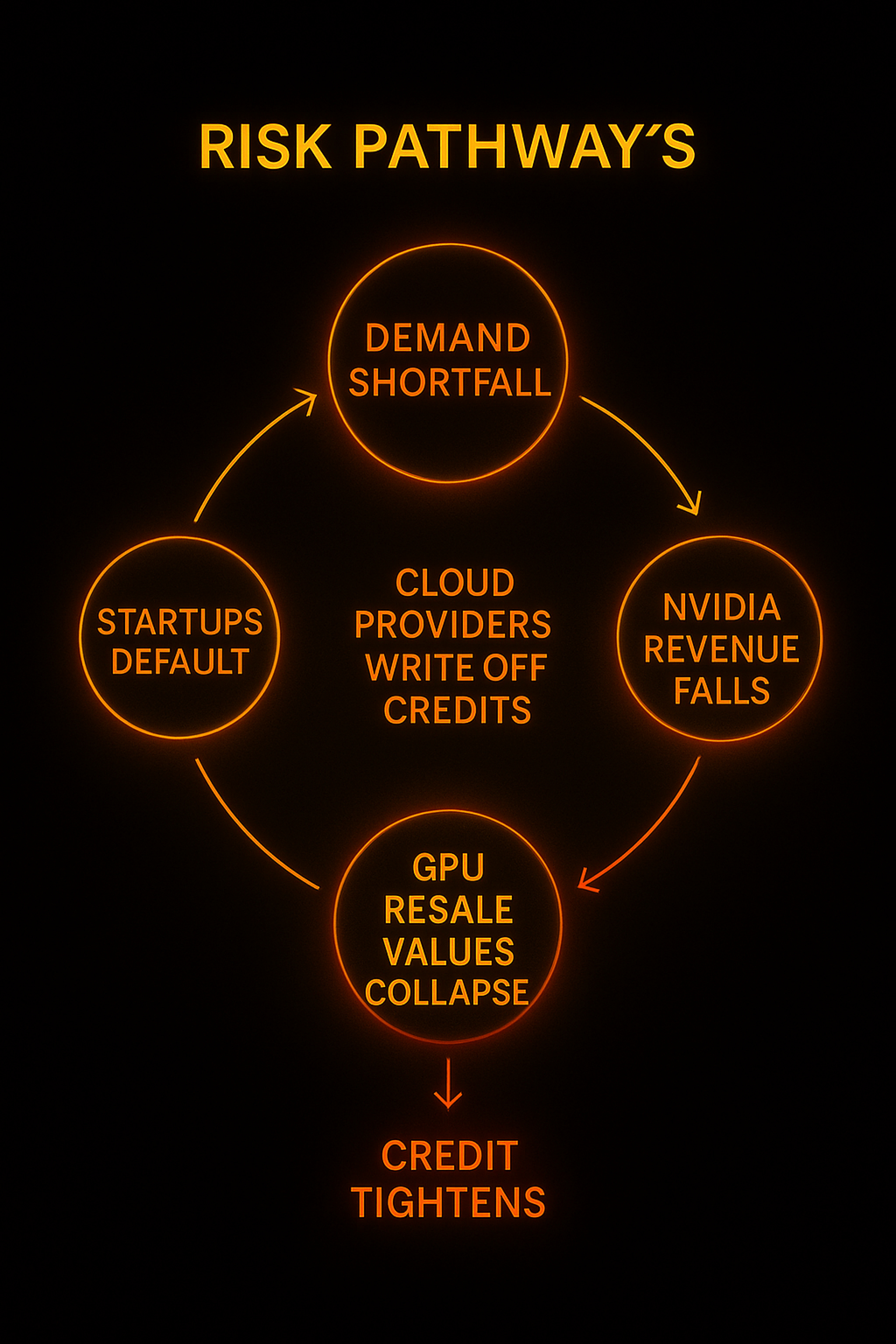

Risk 1: Demand Shortfall (Medium probability, High impact)

Capabilities plateau; adoption lags; willingness to pay disappoints.

Breaks: startup revenues, cloud capacity utilisation, NVIDIA’s customer base; GPU collateral values sink.

Contagion: defaults → write-offs → revenue collapse → resale crash → tighter credit.

Parallel: Fibre glut (1999–2001)—demand arrived years late.

Risk 2: Technological Disruption (Medium-High probability, Very high impact)

10× algorithmic efficiency or new architectures strand current GPUs.

Breaks: installed bases, ABS collateral, leverage.

Parallel: Mainframe → PC transition—rapid value flip.

Risk 3: Regulatory Shock (Low-Medium probability, High impact)

Safety rules raise training costs; antitrust unpicks vertical plays.

Breaks: models predicated on today’s regime; ecosystem strategies.

Parallel: Utility Holding Company Act (1935).

🔄 The Circularity Question: A Precise Definition

True circularity would be: NVIDIA lends to OpenAI → OpenAI buys NVIDIA chips → NVIDIA books revenue → uses it to lend more to OpenAI → repeat. That’s a closed loop—dangerous.

Reality: External capital enters throughout (Microsoft, SWFs, etc.). What we have is strategic interdependence and correlated exposure, not a sealed loop. The systemic risk is concentration on the same underlying bet.

Analogy: 2008 wasn’t “circular finance”; it was correlated housing exposure.

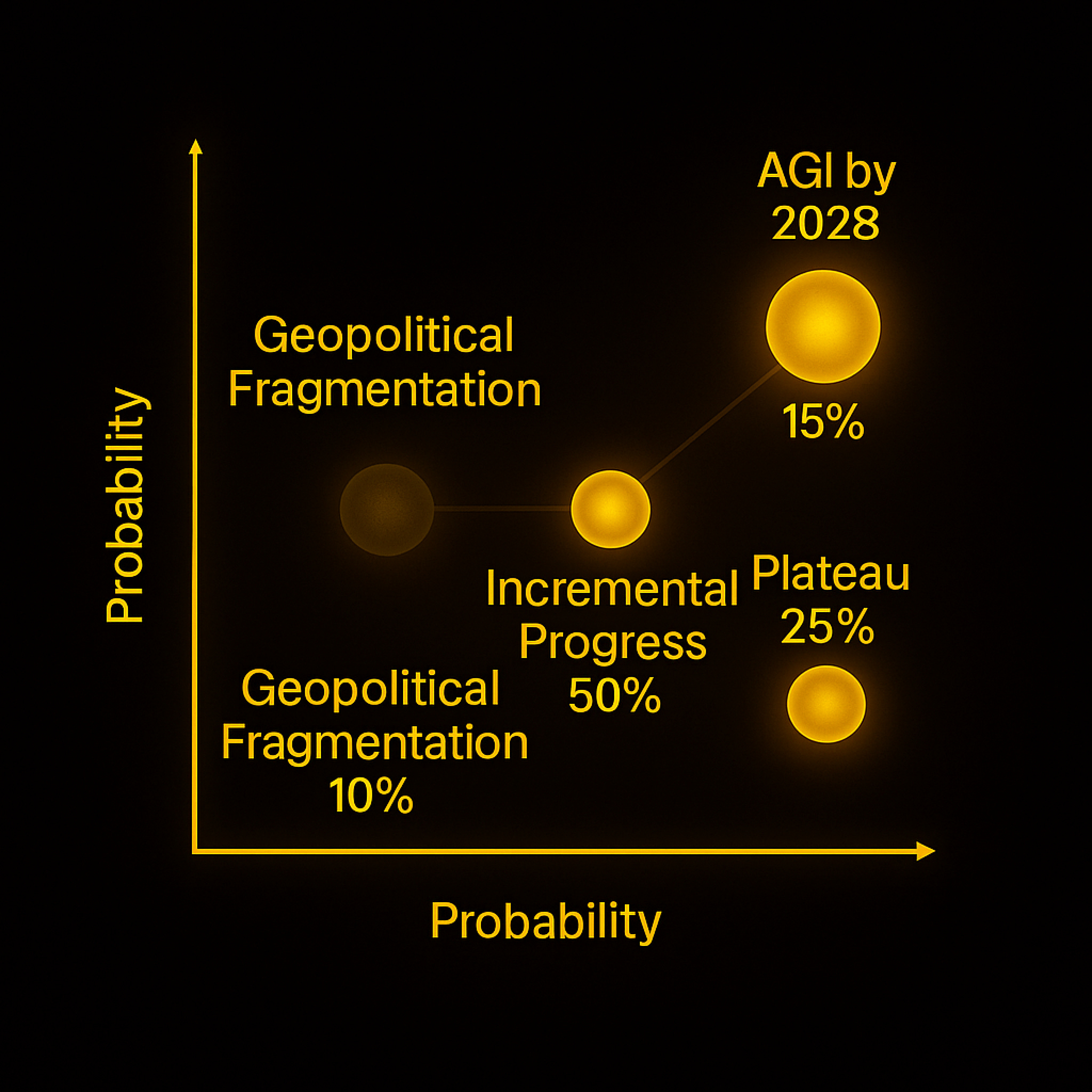

🔭 The Big Question: What Happens When the Loop Breaks?

AGI by 2028 (15%) — Trillions unlocked; infra was under-built.

Incremental Progress (50%) — Steady gains; 2027–28 correction, not catastrophic.

Plateau + Efficiency (25%) — Demand craters; severe correction; leveraged players default.

Geopolitical Fragmentation (10%) — Regional stacks; stranded assets in some markets become strategic.

📊 Key Variable to Watch

Debt-to-GPU-value ratio. If >2:1, the system is over-leveraged.

How to track:

GPU resale values (H100/Blackwell)

Credit downgrades (CoreWeave, Oracle)

Data-centre utilisation (≥80% vs idle)

✅ Key Takeaways

Separate the mechanisms: strategic ecosystem (low risk), vendor financing (medium), asset-backed lending (low circularity/high stranded-asset risk).

Steelman the case: coordination + information advantages can justify circular capital.

Real risks: demand shortfall, tech disruption, regulatory shock.

Precision on “circular”: it’s interdependence and correlation, not a closed loop.

Scenarios: soft landing (30%), boom-bust-prosper (50%), systemic crisis (20%).

This is Part 1 of 5 in the Great AI Infrastructure Build-Out of 2025.

Coming up:

Thank you for reading. If you liked it, share it with your friends, colleagues and everyone interested in the startup Investor ecosystem.

If you've got suggestions, an article, research, your tech stack, or a job listing you want featured, just let me know! I'm keen to include it in the upcoming edition.

Please let me know what you think of it, love a feedback loop 🙏🏼

🛑 Get a different job.

Subscribe below and follow me on LinkedIn or Twitter to never miss an update.

For the ❤️ of startups

✌🏼 & 💙

Derek