🎯 The Thesis in Three Sentences

AI infrastructure faces continuous margin collapse as GPUs obsolete every 2-4 years (not 20-50 years like railways or fiber), fundamentally changing who wins and who loses.

Infrastructure players—NVIDIA, cloud providers, CoreWeave—see this coming, which is why they’re desperately pivoting to applications and software even as they build more hardware.

This creates a golden opportunity for application builders: you benefit from continuously falling costs while infrastructure investors face margin compression. The question isn’t whether to build—it’s how to position correctly.

⚡ The Core Insight: Infrastructure Margins Collapse, Applications Capture Value

Everyone wants this to be like the railway boom of the 1840s. Infrastructure gets built ahead of demand, investors lose money in a spectacular crash, but society benefits from the tracks left behind. The railways enabled the Industrial Revolution. The fiber optic cables laid during the dot-com boom enabled Web 2.0.

The comparison is instructive, but not in the way people think.

A railway line built in 1850 was still carrying trains in 1950 (100-year useful life). Railway companies faced one buildout, then decades of stable operations. Margins were sustainable.

A fiber optic cable laid in 2000 still carries internet traffic today (25-year useful life). Telecom companies laid cable once, then operated it for decades. Infrastructure held value.

But a GPU cluster built in 2023 with H100 chips? Already being replaced by Blackwell in 2025 (2-year cycle for cutting-edge work). Retains maybe 30-50% of value for inference and secondary workloads, but the training premium vanishes. Infrastructure companies must constantly rebuild on depreciating assets. Margins compress continuously.

This changes who wins.

Infrastructure investors face permanent margin erosion. Every GPU generation obsoletes the previous one. Capital expenditure never stops, but pricing power continuously erodes as newer, better hardware floods the market.

Application builders capture permanent margin expansion. Your costs fall continuously. Model API prices that cost $10 per million tokens today will cost $1 in three years and $0.10 in six years. Your margins expand automatically, year after year, with zero effort.

And here’s the part that makes this series different: infrastructure players know this. That’s why they’re moving to your layer.

🔄 Why Infrastructure Players Are Pivoting to Applications

Pay attention to what NVIDIA is actually doing.

They’re not just selling GPUs. They’re investing in 50+ AI startups. Building software platforms. Moving up the stack toward applications and distribution. The world’s most successful infrastructure company is pivoting away from pure infrastructure plays.

OpenAI isn’t satisfied being an API provider. They built ChatGPT—a consumer application with 100 million users. They’re racing to own distribution, not just sell compute.

Microsoft isn’t content providing Azure infrastructure. They bundled Copilot into Office, embedding AI directly into applications.

Why? Because they see two trends:

First, continuous margin compression (happening now): Infrastructure margins compress as hardware obsoletes every 2-4 years. This is structural. It never stops.

Second, potential acute crisis (2027-2029): Debt maturities cluster. Overleveraged players face refinancing risk. GPU utilization might drop. This could trigger rapid correction.

For infrastructure investors, both trends are terrible. For application builders, both trends are excellent.

🗺️ What Each Part Actually Covers

Part 1: The Trillion-Dollar Loop—How It’s Financed

We examine three financing mechanisms:

Strategic ecosystem investment (Microsoft-OpenAI): Rational coordination

Vendor financing (NVIDIA investing in customers): Medium risk, historically questionable

Asset-backed lending (CoreWeave’s $14.5B GPU loans): High stranded asset risk

Key insight: These financing structures aren’t inherently problematic (they’re how infrastructure always gets built), but they create correlated exposure. When combined with fast depreciation, this matters.

Key variable: Debt-to-GPU-value ratios. If >2:1, overleveraged.

Part 2: The New Compute Cold War—Geopolitics

We analyze sovereign AI strategies:

US export controls: Porous and failing (Chinese firms getting 1M+ chips via gray markets)

China’s self-reliance: Rational long-term, but short-term inefficiency

Middle East: Buying GPUs ≠ AI capability (no talent, no ecosystem)

Europe’s caution: Actually smart (avoiding stranded assets)

Key insight: Hardware doesn’t equal capability. Talent and institutions matter more.

Key variable: GPU gray market prices in Singapore, Malaysia.

Part 3: Financial Forensics—Who Survives?

We rank tech giants by risk-adjusted positioning:

Tier 1 (Smart Money):

NVIDIA (9/10): Already pivoting to software/applications via 50+ startup investments

Apple (8.5/10): Not playing = maximum optionality

Tier 2 (Rational Bets):

Microsoft (7.5/10): Generating real AI revenue, but locked into OpenAI

Amazon (7.5/10): Platform play, latecomer risk

Tier 3 (High Risk):

Google (6.5/10): $85B defending search

Meta (6/10): High spending, zero direct revenue

Tier 4 (Moonshots):

OpenAI (4/10): $450B bet on AGI, needs 9-18× revenue growth

Oracle (3/10): $100B in debt, 85% probability of failure

Key insight: Even NVIDIA (the infrastructure winner) is diversifying into applications. That’s validation.

Key variable: OpenAI revenue. Needs $20B+/year by 2026.

Part 4: This Isn’t Railways—Why Depreciation Changes Everything

We analyze why fast depreciation destroys the historical parallel:

Good bubble indicators: 0/3 (infrastructure doesn’t last)

Bad bubble indicators: 5/5 for infrastructure investors

But here’s the twist: The same dynamics that make infrastructure a bad investment make applications an excellent opportunity.

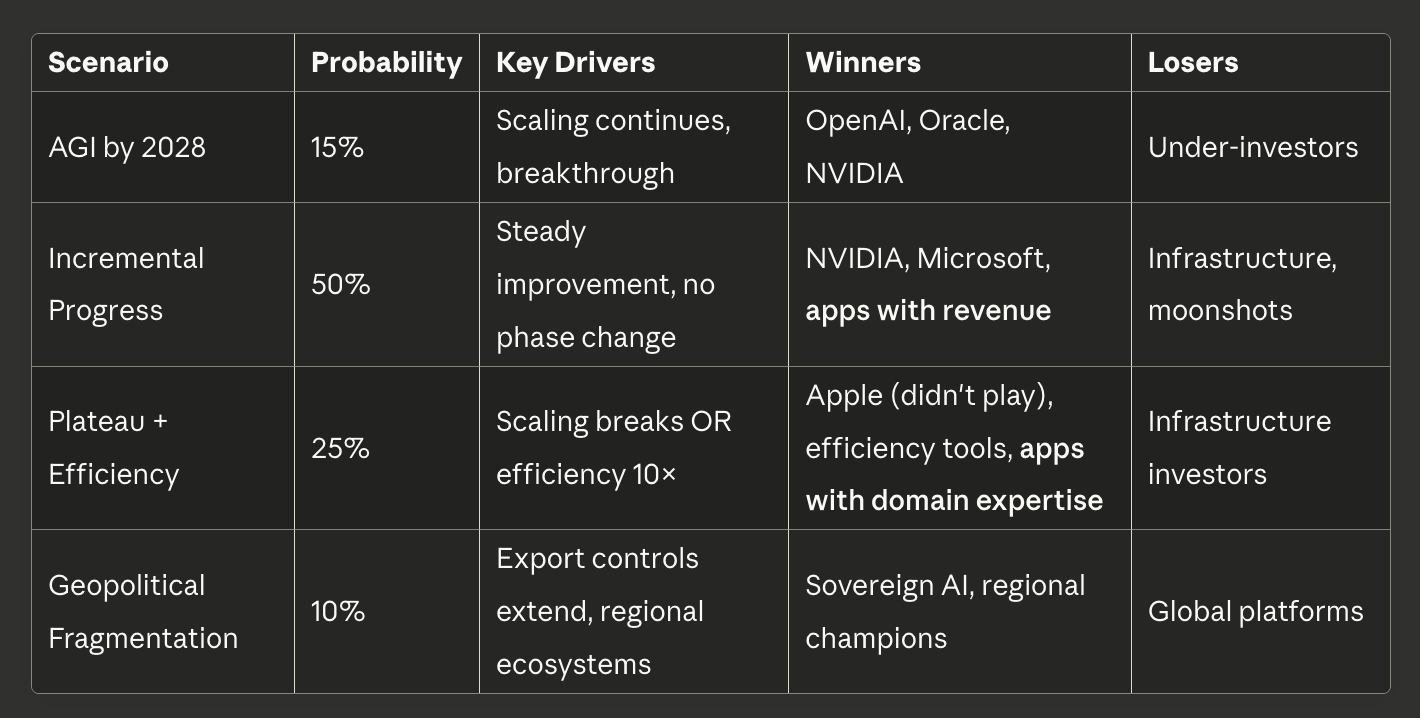

Five scenarios:

AGI by 2028 (15%): You benefit if positioned correctly

Incremental progress (50%): Application margins expand continuously

Capabilities plateau (25%): Domain expertise > AI hype

Efficiency gains 10× (10%): Your COGS drop 90%, margins explode

Key insight: Application builders win in 85%+ of scenarios.

Key variable: GPU resale values, inference API pricing trends.

Part 5: The Application Layer Playbook—Why You Should Build

This is where the series pivots. Parts 1-4 document why infrastructure is problematic. Part 5 explains why that’s good news if you’re building applications.

For application builders:

Continuous margin expansion as costs fall 10× over 5 years

If acute crisis hits (2027-2029), even better: costs crater suddenly, acquire distressed competitors, hire talent at discounts, competition clears out

Position correctly: get to revenue in 18 months, stay flexible on infrastructure, build on commodity layer

For infrastructure investors:

Continuous margin compression (structural)

Potential acute crisis (debt + overcapacity)

Most should sit out or be extremely selective

The strategy: Build applications on rented, commodity infrastructure. Capture value at the software layer where even infrastructure giants are desperately trying to pivot.

📊 The Consistent Probability Framework

Note: Application builders with strong unit economics win in 85%+ of scenarios.

🎯 Key Variables: Your Dashboard

Track these to know which scenario is unfolding:

1. Inference API pricing (continuous trend)

GPT-4-level performance dropped from $20/M tokens (2022) to $0.07 (2024)

If this continues, your margins expand 10× over 5 years

Watch: Model pricing announcements, new provider launches

2. Debt-to-GPU-value ratios (acute crisis indicator)

If >2:1, overleveraged and vulnerable

Watch: CoreWeave, Oracle debt levels; GPU resale values

3. GPU utilization rates (demand signal)

If <60%, overcapacity confirmed

Watch: Spot pricing, cloud provider discounts

4. NVIDIA’s application investments (where smart money moves)

Already 50+ deals in 2025

Watch: Which application categories they’re betting on

5. OpenAI revenue growth (AGI scenario tracker)

Needs $20B+/year by 2026 to justify infrastructure

Watch: ChatGPT subscribers, enterprise deals

👥 Who This Series Is For!

Application Builders (you should read this):

Should you build AI applications? Yes, with discipline

How to position for infrastructure trends? (Build on commodity layer, capture margin expansion)

What happens if correction hits? (Even better for you—costs crater, acquire competitors)

Infrastructure Investors (this explains your risk):

Should you invest in infrastructure? Mostly no, very selective

How to position? (Sit out or <10% to NVIDIA/Apple, prefer application layer)

What’s your risk? (Continuous margin compression + potential acute crisis)

Founders Building Tools/SaaS:

Where should you build? (Application layer, developer tools, vertical SaaS, knowledge platforms)

How fast must you move? (18-month revenue rule)

How to capture falling costs? (Model-agnostic architecture, managed services)

Policymakers:

How to prevent 2008-style contagion? (Monitor debt ratios, prepare restructuring)

Are export controls working? (No—failing, pivot to talent retention)

⚖️ The Synthesis: Two Different Conclusions

For infrastructure investors: Sit this out or be extremely selective. Continuous margin compression plus potential acute crisis creates terrible risk-reward. Even NVIDIA sees this, which is why they’re pivoting to applications.

For application builders: Build now with discipline. You benefit from the exact same trends that hurt infrastructure investors. Continuous cost deflation expands your margins. If acute crisis hits, you benefit even more.

The key insight: Infrastructure stress (continuous or acute) transfers value from hardware to software, from infrastructure to applications. Position accordingly.

⭐ What Makes This Analysis Different

Most AI infrastructure analysis asks: “Is this a bubble?” or “Will AGI happen?”

This series asks: “Given that infrastructure margins compress continuously AND there’s potential acute crisis risk, who benefits and who loses?”

The answer: Application builders benefit. Infrastructure investors lose (except NVIDIA, who’s already pivoting).

Parts 1-4 document the infrastructure stress. Part 5 explains why that’s your opportunity if you’re building applications.

Now let’s dive in...

This is Part 0 of a 5-part series on the Great AI Infrastructure Build-Out of 2025.

The full series:

Thank you for reading. If you liked it, share it with your friends, colleagues and everyone interested in the startup Investor ecosystem.

If you've got suggestions, an article, research, your tech stack, or a job listing you want featured, just let me know! I'm keen to include it in the upcoming edition.

Please let me know what you think of it, love a feedback loop 🙏🏼

🛑 Get a different job.

Subscribe below and follow me on LinkedIn or Twitter to never miss an update.

For the ❤️ of startups

✌🏼 & 💙

Derek

This article comes at the perfect time. You nail the GPU obsolesence. Applications win, thankfully.

A thought on Nvidia's V Michael Burry's chip depreciation argument and why Nvidia are wrong.

The reason older chips appear to have long useful lives right now isn’t because they’re economically efficient. It’s because the supply chain is so constrained that people will run anything they can get their hands on.

That’s not a strategy. It’s a shortage, and right now they can take advantage of it and depreciate old chips over a longer period.

As soon as supply catches up — and especially as AI moves into real-world robotics — the myth collapses. Robotics, automation, AV systems, edge devices… they all need much faster, low-latency inference than 7nm or 14nm silicon can deliver.

The reality is simple:

Older nodes persist today because we have a bottleneck, not because they’re good enough.

Once AI leaves the cloud and enters physical systems, inference becomes the new frontier, and efficiency wins.

The obsolescence cycle accelerates, not slows.

The industry hasn’t priced this in yet. But robotics will force it.